Retailers who accept both EBT and credit or debit cards are operating across two distinct payment systems simultaneously. Each has its own fee structure, compliance requirements, and risk exposure. Understanding how both work at the processing level helps retailers manage costs, avoid violations, and build a checkout experience that works for every customer.

How Processing Fees Work for Each Payment Type

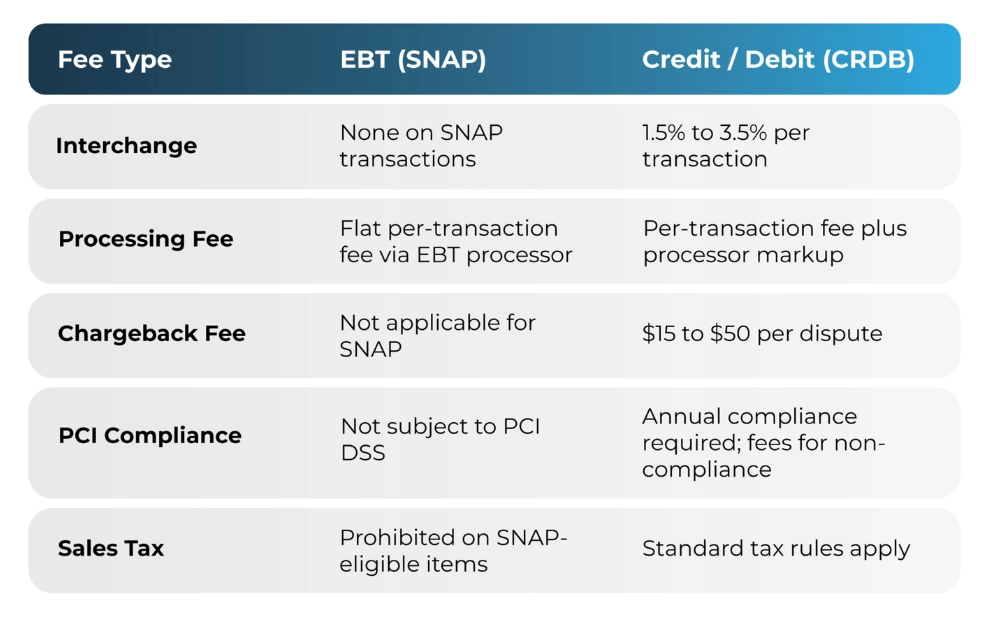

Credit and debit transactions (CRDB) are built on a multi-party fee model. Every CRDB transaction generates an interchange fee paid to the card-issuing bank, typically ranging from 1.5% to 3.5% of the transaction value depending on the card type. Rewards cards, commercial cards, and premium credit cards all carry higher interchange rates. On top of that, merchants pay a processor markup, gateway fees, and in some cases monthly software or network access fees. CRDB also exposes merchants to chargeback fees of $15 to $50 per dispute, plus the potential loss of the transaction amount if the dispute is not won.

SNAP EBT transactions operate outside the interchange system entirely. There is no issuing bank taking a percentage cut, so merchants pay a flat per-transaction fee set by their EBT processor rather than a percentage of the sale. This makes SNAP one of the lower-cost payment types to process on a per-transaction basis. EBT also carries no chargeback exposure under the standard card network dispute process, which reduces a common source of financial risk for CRDB merchants.

WIC transactions sit closer to the CRDB model in terms of cost. They carry processing fees that vary by state and processor, and they involve item-level approval tied to a state-specific approved product list. Retailers accepting WIC should confirm their fee structure with their processor directly.

Compliance Obligations Are Different in Kind

CRDB compliance centers on PCI DSS, the Payment Card Industry Data Security Standard enforced by card networks. Merchants complete annual self-assessments or audits, maintain network security requirements, and follow cardholder data handling protocols. Non-compliance results in monthly fees from your processor, and a data breach while non-compliant can trigger significant fines from card networks. These are meaningful obligations, but they are managed primarily through your processor relationship.

EBT compliance is a federal regulatory obligation tied to your USDA SNAP authorization, and the consequences of violations are more severe. The USDA Food and Nutrition Service can suspend or permanently disqualify retailers from the SNAP program for violations, and civil monetary penalties can reach $100,000 per infraction. Unlike a PCI fine, SNAP disqualification directly impacts a retailer’s ability to serve customers who rely on those benefits.

Core SNAP compliance requirements every authorized retailer must follow:

- Item eligibility enforcement: SNAP-ineligible items cannot be tendered on EBT. Misconfigured item flags in your POS are treated the same as intentional violations under USDA enforcement.

- No sales tax on eligible items: Applying sales tax to SNAP-eligible food items during an EBT transaction is a federal violation, not just a checkout error.

- Receipt requirements: Every completed EBT transaction must include the customer’s remaining SNAP balance on the printed receipt, a requirement that has no equivalent for CRDB transactions.

- No surcharging: Retailers cannot add fees or surcharges for EBT transactions. Minimum purchase thresholds that effectively penalize EBT customers are also restricted under federal rules.

- Recordkeeping: SNAP transaction records must be retained for a minimum of two years and made available to the USDA upon request.

Two Compliance Tracks Running at the Same Time

Retailers accepting both payment types are managing PCI DSS requirements for CRDB and USDA FNS requirements for EBT simultaneously. An integrated payment platform that keeps these environments properly separated and handles reporting for both significantly reduces that administrative burden.

The Risk Profiles Point in Different Directions

CRDB carries ongoing financial dispute risk in the form of chargebacks. Any cardholder can dispute a transaction through their issuing bank, triggering a formal process that can result in the merchant losing the transaction amount plus a chargeback fee. High dispute rates can lead to elevated processing costs or account termination. Managing chargeback risk is a standard part of running CRDB payments.

EBT carries minimal chargeback exposure since there is no card network dispute process for SNAP transactions. However, the regulatory risk is more significant. A USDA compliance investigation finding a pattern of ineligible item sales, incorrect tax application, or other violations can result in disqualification from the SNAP program entirely. The risk profiles are essentially inverted: CRDB risk is transactional and financial, while EBT risk is regulatory and structural.

Understanding both risk profiles matters when choosing a payment processor and POS platform. The right solution should address CRDB chargeback management and EBT compliance enforcement as separate but equally important functions.

Why Accepting Both EBT and CRDB Strengthens Your Business

Accepting both EBT and credit/debit (CRDB) payments is not just about flexibility at checkout, it is a strategic advantage that directly impacts revenue, customer reach, and long-term stability. Each payment type serves a different segment of your customer base, and together they create a more resilient business model.

EBT allows retailers to tap into a consistent and essential spending category. SNAP benefits are distributed monthly, creating predictable foot traffic and recurring purchases. For many retailers, especially in grocery, convenience, and quick-service environments, EBT transactions represent a stable revenue stream that is less sensitive to economic fluctuations.

CRDB, on the other hand, enables higher average ticket sizes and broader purchasing flexibility. Customers using credit and debit cards are not limited to eligible items, which increases basket size and allows for more discretionary spending. Additionally, CRDB supports modern checkout expectations, including contactless payments, mobile wallets, and online ordering integrations.

When combined, EBT and CRDB create a balanced payment ecosystem. EBT drives consistent volume and customer loyalty, while CRDB drives margin expansion and transaction growth. Retailers that support both are better positioned to serve their entire community, reduce missed sales opportunities, and optimize overall performance at the point of sale.

One Platform for Both Payment Types

Managing EBT and CRDB through disconnected systems creates reporting gaps, reconciliation headaches, and a higher chance of compliance errors across both payment types. An integrated platform handles SNAP item eligibility, compliant receipts, split tender, chargeback management, and consolidated settlement reporting in one place.

goEBT helps retailers accept SNAP EBT, credit and debit, OTC benefits, healthy food benefits, and more through a single platform built to handle the requirements of each payment type correctly. Contact one of our experts today to simplify your payment processing and stay compliant across the board.